Financial education is defined as the knowledge and skills needed to make informed, confident decisions about money. For young people, building this foundation early is the difference between entering adulthood prepared or perpetually playing catch-up. Programs like FDIC Money Smart and Talk Money have already demonstrated measurable gains in student confidence and financial behavior. The stakes are real: U.S. adults answer only 49% of basic financial literacy questions correctly, a figure that has barely moved in a decade. That number tells you the current system is not working. Starting earlier, and smarter, is the fix.

Why financial education matters for youth outcomes

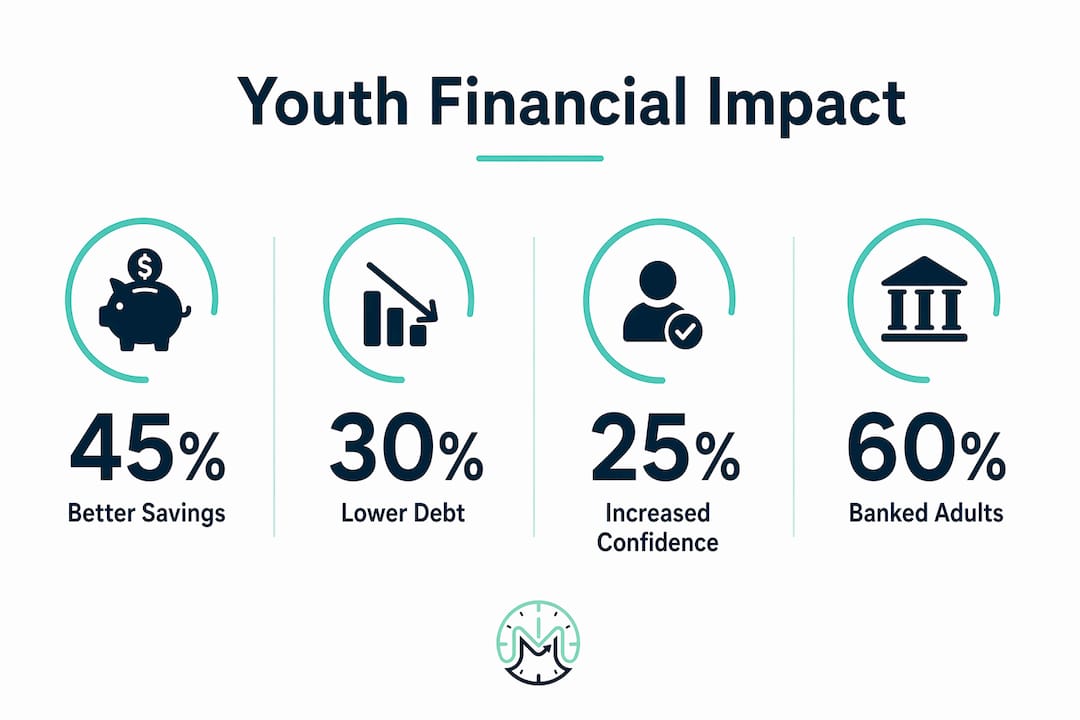

Financial literacy, the recognized term for the skills and knowledge covered here, does more than teach teens to balance a checkbook. Research from the FDIC shows that high school finance coursework directly reduces the likelihood of being unbanked as an adult. Students who took a personal finance class were less likely to avoid or distrust banking institutions later in life. That is a behavioral shift, not just a knowledge gain.

"Early financial education shapes confidence and engagement with financial institutions, reducing adult unbanked rates." — FDIC, 2026

The Kansas City Fed reinforces this point. Their programs link classroom financial simulations to real-world decisions, showing that students who practice financial reasoning in context are more motivated and retain more. Engagement, not just exposure, drives the outcome.

The knowledge gap among adults is not random. It reflects a generation that never received structured money education during their formative years. Low financial literacy doubles debt constraints and multiplies the likelihood of having no emergency savings by five times. Those are not abstract statistics. They describe real households struggling with avoidable financial stress.

Why knowledge alone is not enough

Teaching facts about compound interest does not automatically change behavior. FDIC research confirms that effective youth programs build attitudes and behavioral intentions, not just definitions. A student who understands why saving matters and feels capable of doing it is far more likely to open a savings account at 18 than one who memorized the formula for interest. Confidence and perceived relevance are the real levers.

| Outcome Measured | Impact of Youth Financial Education |

|---|---|

| Adult unbanked status | Reduced among students with high school finance coursework |

| Emergency savings | Low literacy linked to 5x higher likelihood of no savings |

| Debt constraints | Low literacy doubles debt-related financial stress |

| Banking confidence | Early education increases engagement with financial institutions |

What teaching methods actually work for students

Not all financial education is created equal. A 2026 randomized controlled trial published in Frontiers in Education compared project-based learning (PBL) to standard instruction for middle school financial literacy. Project-based learners scored 6.65 on post-tests versus 5.64 for the standards-based group. That gap reflects a meaningful difference in how well students could apply what they learned, not just recall it.

The reason PBL works is straightforward. When students make real decisions, like planning a mock budget for a first apartment or comparing loan terms for a used car, they practice the reasoning they will actually need. Authentic financial decisions build comprehension and vocabulary in ways that passive lectures simply cannot match.

Here is what the most effective youth financial education programs have in common:

- Decision-focused tasks. Students practice choosing between options, not just defining terms.

- Relevant scenarios. Topics connect to real choices teens face: part-time job income, college costs, first credit cards.

- Short, repeatable sessions. PBL interventions work even in brief formats, making them scalable for busy classrooms.

- Confidence-building feedback. Programs that track progress and celebrate small wins keep students engaged longer.

The Talk Money program in Australia reached over 530,000 students and produced striking results. Participants showed a +40% increase in confidence managing money and a +35% increase in intent to achieve financial goals. Confidence is the outcome that compounds over time.

Pro Tip: If you are a student looking to build money skills fast, prioritize programs that ask you to make decisions, not just read definitions. Simulations, budgeting exercises, and goal-setting tools will teach you more in one hour than a textbook chapter will in three.

What financial skills should youth learn and when?

The FDIC's Money Smart for Young People curriculum covers Pre-K through 12th grade, with the high school version containing 22 structured lessons on real-world topics including college financing, car ownership, and renting a first home. That scope reflects a core principle: financial concepts should be introduced when they are relevant, not all at once.

Here is a practical breakdown of what to learn at each stage:

- Middle school (ages 11 to 14): Needs vs. wants, saving goals, basic budgeting, understanding a paycheck

- Early high school (ages 14 to 16): Checking and savings accounts, interest rates, credit basics, comparing prices

- Late high school (ages 16 to 18): Credit scores, student loans, tax basics, investing fundamentals like index funds and ETFs

- College (ages 18 to 22): Debt management, renter's insurance, building an emergency fund, retirement accounts like a Roth IRA

Why sequencing matters

Introducing investing to a 12-year-old who has never managed a budget creates confusion, not capability. Developmentally sequenced education reduces abstraction and keeps concepts grounded in decisions students are actually making. A 16-year-old with a part-time job understands taxes and saving in a way a 10-year-old simply cannot.

| Stage | Core Skills | Why It Matters Now |

|---|---|---|

| Middle school | Budgeting, saving, needs vs. wants | Builds foundational habits before spending pressures increase |

| High school | Credit, debt, banking basics | Prepares for first financial accounts and part-time income |

| College | Loans, investing, emergency funds | Directly relevant to decisions made in real time |

The goal is not to turn every student into a financial expert. The goal is to make sure no one graduates high school without knowing how credit scores work, what compound interest costs them in debt, or how to build a basic monthly budget. Those three skills alone would change millions of financial trajectories.

How financial knowledge improves your life and community

Financial education does not just protect you from bad decisions. It actively builds the life you want. Students who develop money management skills early are more likely to set savings goals, engage with banks and credit unions, and make informed choices about borrowing. That confidence compounds just like interest does.

The community impact is real too. Young people who understand personal finance are more likely to participate in local economies responsibly. They open accounts, build credit, avoid predatory lenders, and eventually invest. Each of those behaviors strengthens the financial ecosystem around them.

Here is what applying financial education looks like in practice:

- Setting a savings goal for a specific purchase instead of impulse spending

- Comparing interest rates before accepting a credit card offer

- Understanding the true cost of a student loan before signing

- Talking openly about money with family, which research links to better financial outcomes for the whole household

- Using free tools and apps to track spending and build habits

Pro Tip: Start the money conversation at home. Research shows that financial conversations at home significantly improve young people's financial confidence and decision-making. You do not need a finance degree to talk about budgets, goals, and trade-offs with the people around you.

Peer influence also plays a role. When financial literacy becomes a normal topic among friends, students are more likely to share strategies, ask questions, and hold each other accountable. That social layer is one reason programs like Reality Fairs, run by the Kansas City Fed, are so effective. They make money decisions feel normal and worth discussing.

Key takeaways

Financial education matters for youth because it builds the confidence, habits, and knowledge that directly shape adult financial stability, banking participation, and resilience against debt.

| Point | Details |

|---|---|

| Start early, sequence well | Introduce concepts when relevant to avoid disengagement and build real skills progressively. |

| Behavior beats knowledge | Programs that build confidence and intent, not just facts, produce lasting adult financial outcomes. |

| Project-based learning wins | PBL students outperform peers on application tasks, scoring higher in budgeting and decision-making. |

| Gaps are costly | Low financial literacy doubles debt stress and multiplies the risk of having no emergency savings. |

| Community impact is real | Financially educated youth engage with banks, avoid predatory products, and strengthen local economies. |

Build your money skills with Minutementor

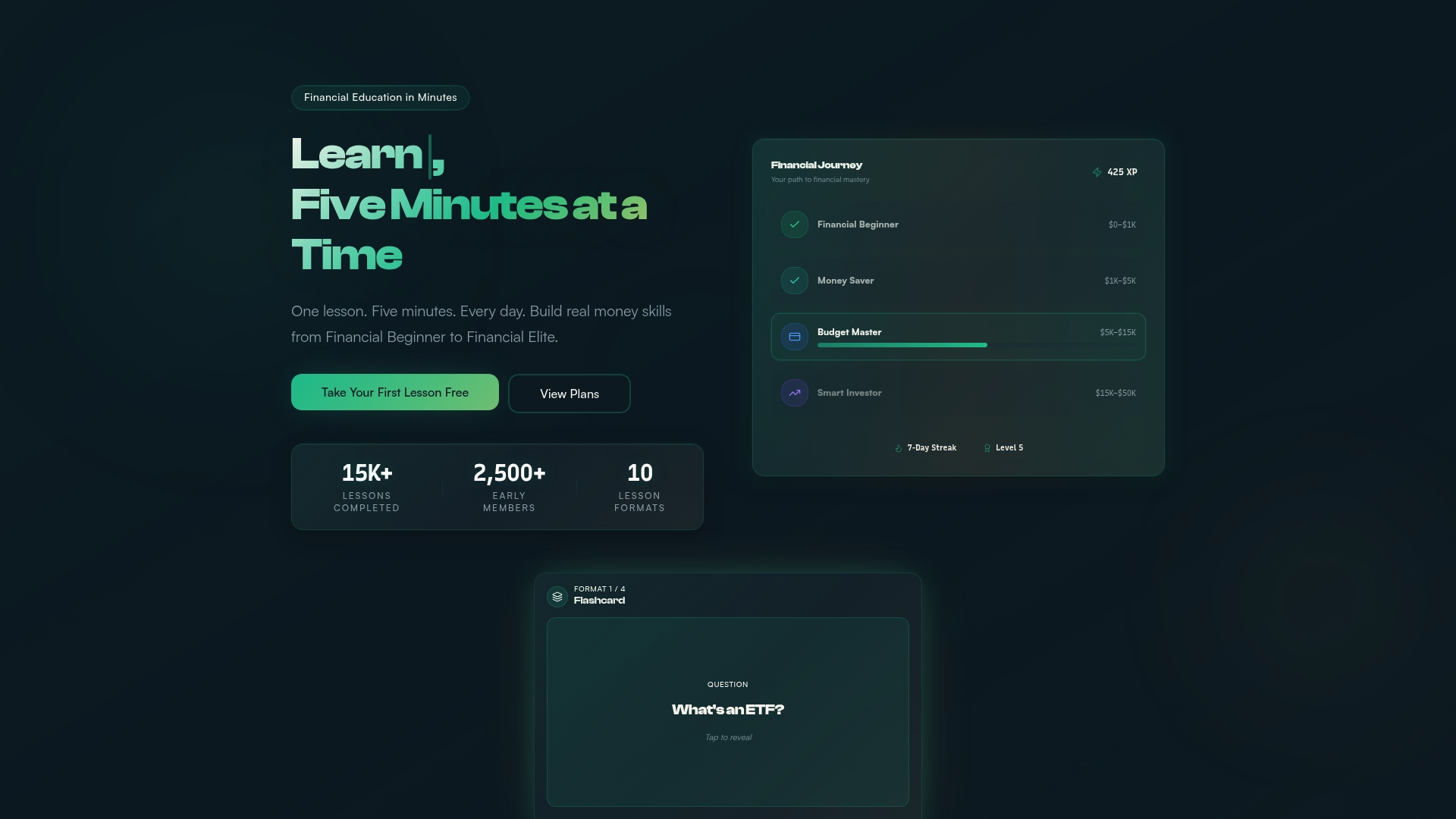

You do not need a semester-long course to get financially confident. Minutementor delivers targeted financial lessons in five minutes a day, built specifically for students and young professionals who want real skills without the overwhelm.

The platform's AI-powered coach tailors your learning path to your actual goals, whether that is building a budget, understanding credit, or starting to invest. Lessons are short, interactive, and designed to fit into your day, not take it over. Students have used Minutementor to save thousands and hit financial milestones they thought were years away. Start learning today and see how fast five minutes a day adds up. Check out Minutementor's pricing to find the plan that fits your goals.

FAQ

Why does financial education matter for young people?

Financial education gives young people the skills and confidence to make smart money decisions before the stakes get high. FDIC research shows that students who take personal finance courses in high school are less likely to be unbanked and more likely to engage with financial institutions as adults.

What financial skills should teenagers learn first?

Teenagers should start with budgeting, saving, and understanding needs versus wants before moving to credit and debt concepts. The FDIC Money Smart curriculum recommends sequencing topics developmentally so each concept builds on real decisions students are already facing.

Does financial education actually change behavior?

Yes, but only when it goes beyond facts. Programs that build confidence and perceived relevance, like project-based learning and simulation-based curricula, produce measurable shifts in attitudes and financial intentions, not just quiz scores.

How does low financial literacy affect young adults?

Low financial literacy doubles debt constraints and significantly increases the likelihood of having no emergency savings. The 2025 TIAA-GFLEC Personal Finance Index found that U.S. adults correctly answered only about 49% of basic financial literacy questions, a figure that has remained flat for nearly a decade.

What is the best way for students to learn personal finance?

Project-based learning, simulations, and short daily practice sessions outperform traditional lecture formats. Programs like Talk Money and FDIC Money Smart, combined with tools like Minutementor, give students both the structure and the motivation to build lasting money habits.