Automated investing is defined as scheduling regular, fixed contributions from your paycheck directly into diversified, low-cost portfolios without manual intervention. For any young professional looking to automate investments, this approach removes two of the biggest wealth killers: emotional decision-making and inconsistent contributions. Platforms like Vanguard, Fidelity, and Schwab have made this process accessible in under 30 minutes. Financial experts recommend automating 10-15% of gross income into index funds or robo-advisors as the single most reliable path to long-term wealth building. The earlier you start, the harder compounding works for you.

How to automate investments as a young professional

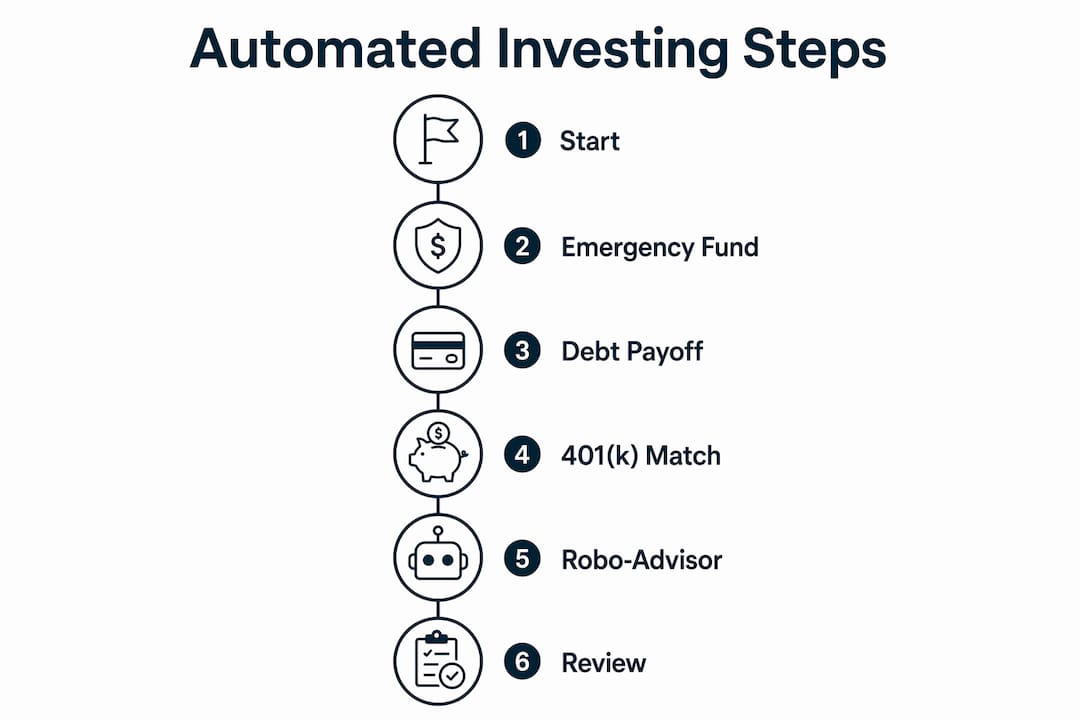

Before you touch a single investment account, your financial foundation needs to be solid. Automation works best when it runs without interruption, and two things will interrupt it fast: high-interest debt and a missing emergency fund.

High-interest debt above 7% APR should be paid off aggressively before you invest heavily. Any debt above that threshold is essentially a guaranteed negative return on your money. For lower-interest debt like federal student loans, pay the minimum and invest the rest.

Your emergency fund is the shock absorber for your automation. Without three to six months of expenses in a savings account, one unexpected car repair or medical bill forces you to pause contributions or sell investments at the wrong time. Build that buffer first, even if it takes a few months.

Here is what to prioritize before automating:

-

Pay off high-interest debt (above 7% APR) before directing significant money to investments

-

Maintain minimum payments on lower-interest debt while investing the difference

-

Build a starter emergency fund of at least one month of expenses before automating

-

Capture your full employer 401(k) match immediately. This is free money with a 50-100% instant return, and no index fund can beat it

Pro Tip: If your employer matches 4% of your salary in a 401(k), contribute at least 4% from day one. Skipping the match is the most expensive mistake young professionals make.

What tools and strategies work best for passive investing?

Once your foundation is set, you face one real choice: build your own index fund portfolio or use a robo-advisor. Both work. The right pick depends on how much you want to think about it.

The three-fund portfolio approach

A three-fund portfolio built with VTI (US total market), VXUS (international stocks), and BND (US bonds) is the gold standard for hands-off investors. 90% of active fund managers underperform index funds over 15 years. That single statistic makes the case for passive index investing better than any argument. Expense ratios on these funds sit below 0.1%, meaning you keep nearly all of your returns. Vanguard, Fidelity, and Schwab all offer equivalent funds with zero trading commissions.

Robo-advisors for full automation

Robo-advisors like those offered through Fidelity Go and Schwab Intelligent Portfolios handle contributions, automatic rebalancing, and tax-loss harvesting without you lifting a finger. Robo-advisors automate rebalancing and tax optimization, making them ideal for investors who want zero manual management. The tradeoff is a small management fee, typically 0.25% annually, though some platforms charge nothing below a certain balance threshold.

Here is a direct comparison to help you decide:

| Feature | DIY index funds | Robo-advisor |

|---|---|---|

| Expense ratio | Below 0.1% | 0.25% or less |

| Rebalancing | Manual (once per year) | Automatic |

| Tax-loss harvesting | Manual | Automatic |

| Setup complexity | Low to moderate | Very low |

| Best for | Hands-on learners | Full automation seekers |

| Platforms | Vanguard, Fidelity, Schwab | Fidelity Go, Schwab Intelligent Portfolios |

Young investors hold a structural advantage here. Longer time horizons support aggressive, stock-heavy allocations of 80-90% stocks. That means more growth potential over decades, with time to recover from any short-term dips. A 28-year-old can afford to ride out a market correction that would terrify a 58-year-old.

Step-by-step: how to set up automated investing

This is the part most articles skip over. Here is the exact process, in order.

-

Enroll in your employer’s 401(k) or 403(b) plan. Set your contribution to at least the full employer match percentage. Contributions come out of your paycheck before taxes, so you never see the money and never miss it.

-

Open a brokerage account at Vanguard, Fidelity, or Schwab. A Roth IRA is the best starting point for most young professionals under the income limit. Contributions grow tax-free, and you can withdraw them penalty-free in retirement.

-

Set up a recurring automatic transfer from your checking account to your investment account. Aim for the day after your paycheck clears. Target 10-15% of your gross income across all accounts combined.

-

Program automatic purchases of your chosen funds. This step is where most people make a critical error. Money left in a settlement account sits idle and earns nothing. You must confirm that your platform is set to automatically buy your selected funds, not just hold the cash.

-

Enable dividend reinvestment (DRIP). Every dividend your funds pay out gets automatically reinvested into more shares. This compounds your returns without any action on your part.

-

Set a calendar reminder for an annual rebalancing check. Once per year, review whether your allocation has drifted from your target. A 90/10 stock-bond split can shift to 95/5 after a strong market year. Rebalancing brings it back.

-

Activate an auto-increase feature. Many 401(k) plans and some brokerage platforms let you schedule automatic contribution increases. Raising contributions by at least 1% after each salary increase prevents lifestyle creep and accelerates wealth building as your income grows.

Pro Tip: After setting up automation, check your account after the first two or three transfers to confirm money moved AND purchased funds. Then step back. Constant checking is the enemy of good returns.

Here is a quick reference for your automation setup:

| Step | Action | Timing |

|---|---|---|

| 401(k) enrollment | Set contribution to full employer match | Day one at new job |

| Roth IRA transfer | Auto-transfer from checking | Day after payday |

| Fund purchase | Enable automatic buy orders | Same day as transfer |

| DRIP | Enable dividend reinvestment | One-time setup |

| Rebalancing | Review and adjust allocation | Once per year |

| Contribution increase | Raise rate after salary bump | After each raise |

Common mistakes that derail automated investment plans

Automation does the heavy lifting, but it cannot protect you from yourself. These are the behavioral traps that cost young investors the most.

“The investor’s chief problem, and even his worst enemy, is likely to be himself.” — Benjamin Graham

Checking your portfolio too frequently causes anxiety and panic-selling, both of which reduce returns. Experts cap portfolio reviews at once per quarter. Market drops feel catastrophic when you watch them daily. They look like minor blips on a 20-year chart.

Here are the most common pitfalls and how to avoid them:

-

Panic-selling during downturns. Market corrections are normal. Selling locks in losses. Your automated contributions during a dip are actually buying more shares at a discount.

-

Overcomplicating your portfolio. Adding 12 different funds does not reduce risk. It adds confusion and increases the chance you will make a bad decision under pressure. Three funds are enough.

-

Letting automation run on idle cash. Confirm your platform buys funds automatically. Many beginners set up transfers but forget to configure automatic purchases, leaving money sitting in cash for months.

-

Skipping contribution increases. Every raise you get is an opportunity to increase your savings rate. If you do not automate the increase, lifestyle inflation will absorb the extra income within weeks.

-

Stopping contributions during market drops. This is the opposite of what you should do. Consistent contributions through volatility is the entire point of automation.

The discipline to leave your portfolio alone is genuinely hard. Automation makes it easier by removing the daily decision to invest. You already made that decision once. Let it run.

Key takeaways

Automating your investments with low-cost index funds and consistent contributions is the most reliable wealth-building strategy available to young professionals today.

| Point | Details |

|---|---|

| Build your foundation first | Pay off debt above 7% APR and build an emergency fund before automating. |

| Capture the employer match | Always contribute enough to get the full 401(k) match before investing elsewhere. |

| Choose simple over complex | A three-fund portfolio with VTI, VXUS, and BND outperforms most active strategies. |

| Confirm fund purchases | Verify that transfers actually buy funds, not just sit as idle cash. |

| Increase contributions over time | Use auto-increase features to raise your savings rate after every salary bump. |

Why I think most young professionals overcomplicate this

Here is what I have seen over and over: smart, motivated people in their late 20s and early 30s spend months researching the “perfect” portfolio while their savings sit in a checking account earning nothing. The research phase becomes a substitute for action.

The truth is that a three-fund portfolio set up in an afternoon at Fidelity or Vanguard, with automatic contributions and dividend reinvestment enabled, will outperform the vast majority of actively managed strategies over a 30-year horizon. The complexity is not where the returns come from. The consistency is.

What automation actually does is remove the daily vote on whether to invest. Without it, every market headline becomes a reason to wait. With it, your contributions go in regardless of what the S&P 500 did last Tuesday. That behavioral edge compounds just as powerfully as the financial returns.

The one thing I would tell every young professional starting out: do not wait until you have the perfect allocation figured out. Start with a simple target-date fund if nothing else. Get the money moving. Refine later. Time in the market beats time spent optimizing.

— Aryan

Build your investment knowledge with Minutementor

Getting your automation set up is step one. Understanding why it works, and how to adjust it as your income grows, is what separates investors who stay the course from those who bail at the first market dip.

Minutementor delivers five-minute daily lessons on personal finance topics including automated investing, Roth IRA strategy, index fund selection, and debt management. The AI-powered coach at Minutementor tailors your learning path to your specific goals, whether you are just starting your first 401(k) or optimizing a portfolio you have had for years. You can finish a full lesson on your commute. No jargon, no fluff, just the knowledge you need to build real wealth with confidence.

FAQ

What does it mean to automate investments?

Automating investments means scheduling recurring transfers from your bank account into investment accounts, with funds automatically purchasing index funds or ETFs on a set schedule. The goal is consistent, emotion-free wealth building without manual action each month.

How much should a young professional automate into investments?

Financial experts recommend automating 10-15% of gross income across all investment accounts combined. Start with whatever captures your full employer 401(k) match, then build toward that target percentage over time.

What are the best investment apps for beginners starting out?

Fidelity, Vanguard, and Schwab are the top platforms for young professionals because they offer zero-commission trades, automatic investment features, and low-cost index funds. Fidelity Go and Schwab Intelligent Portfolios add robo-advisor automation for fully hands-off investing.

Should I pay off debt before automating investments?

Pay off high-interest debt above 7% APR before investing heavily, since that rate of return is nearly impossible to beat consistently in the market. For lower-interest debt, pay the minimum and invest the rest simultaneously.

How often should I check my automated investment portfolio?

Experts recommend reviewing your portfolio no more than once per quarter. Frequent portfolio monitoring increases anxiety and the likelihood of panic-selling, both of which reduce long-term returns significantly.